“Buy on the fringe and wait. Buy land near a growing city! Buy real estate when other people want to sell. Hold what you buy!” – John Jacob Astor

When investing in real estate, ideally, one hopes to attain benefits such as: a) low acquisition cost, b) limited tenant problems, and, c) steady appreciation. A-B-C. One way to arrive at A-B-C is often overlooked.

A-B-C created America’s first multi-millionaire, John Jacob Astor. However, pursuing a real estate strategy comparable to the one America’s first multimillionaire utilized to become America’s first multimillionaire is not common.

For savvy investors, prioritizing the acquisition of nonperforming properties can be a good route to take. While this is not a process utilized by a majority of owner-occupying home buyers, owning the home you live in correlates to building net worth. For investors. For families.

Equity built up in homes (over time) makes up in excess of 75% of the total net worth for American families.

“Real Estate cannot be lost or stolen, nor can it be carried away. Purchased with common sense, paid for in full, and managed with reasonable care, it is about the safest investment in the world.” – Franklin D. Roosevelt

Identifying nonperforming properties available at great prices…

With regard paid to neighborhood stabilization and community development, land banks play an important role. They acquire – then convey – non-performing properties to those who can transition nonperforming properties into performing properties. Land bank properties can be acquired at prices which are less than market rate prices.

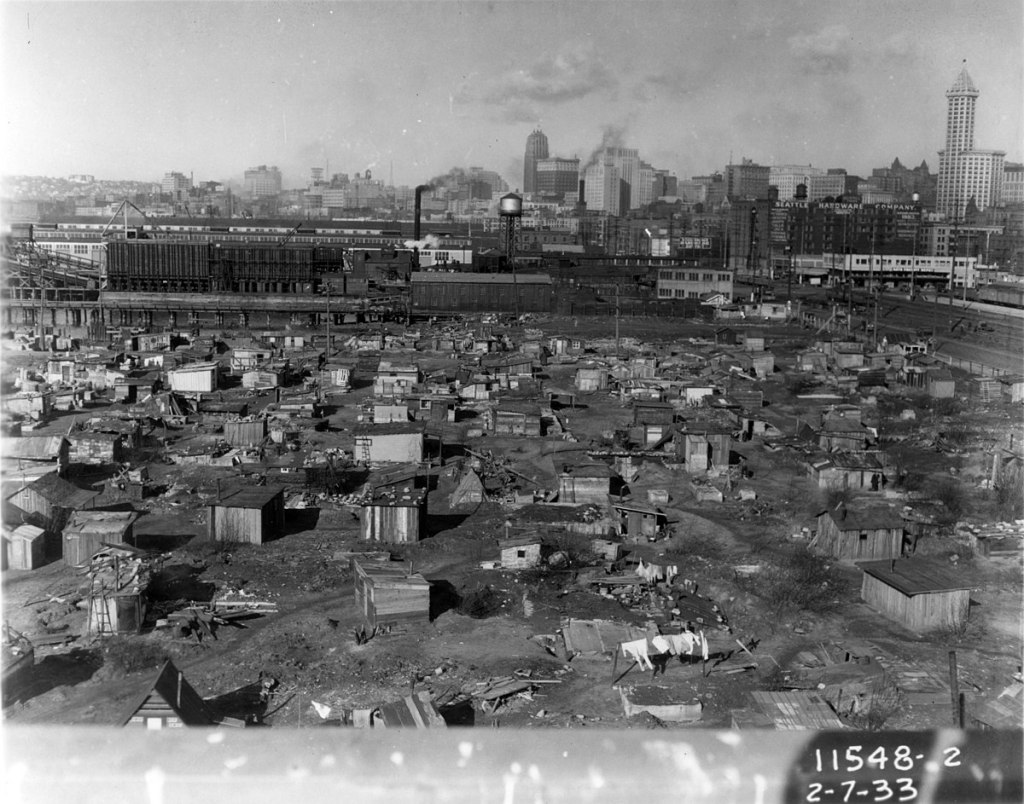

According to a report put forth by the Brookings Institute a few years ago, just about 15% of land in American cities is vacant. Vacant land can be categorized as nonperforming. In that vacant land does not generate property tax revenue. All the while, property taxes function as a vital source of revenue for cities.

Property taxes. A lack thereof?

Reduced property tax receipts impede the sustainability of any city. Reduced property tax receipts are one byproduct of nonperforming properties.

Nonperforming properties…let’s look at St. Louis.

Over the years, St. Louis took possession of in excess of 10,000 nonperforming properties. Residential homes. Vacant lots. Vacant buildings.

By conveying properties the city took possession of to developers, St. Louis alleviated having to operate as a de-facto property manager. Snow removal. Mowing lawns. Boarding up buildings. Tasks transferred in St. Louis to developers.

How so?

Not the conventional way. Neither St. Louis nor land banks use Realtors to sell properties. So let’s look at how St. Louis conveys properties.

Land Reutilization Authority…

The origin for St. Louis’s Land Reutilization Authority – LRA – is found in Title 1 of the Housing and Community Development Act of 1974. In the beginning, funding for the Land Reutilization Authority came through HUD.

The process in St. Louis…

To acquire a Land Reutilization Authority property, buyers complete an Offer To Purchase Form. Buyers submits Offer To Purchase Forms to the LRA, along with two most recent pay stubs, the prior year’s W2 and tax return and the buyer’s most recent bank statement. Buyers also discloses their funding source. A bank. mortgage company. Cash on hand. A Planning Sheet is attached to each buyer’s Offer To Purchase Form.

The Planning Sheet is an overview. The Planning Sheet provides details pertaining to the buyer’s vision for how they plan to improve the property.

The conveyance of city-owned properties and land banks properties happens at the local level. Procedures vary. City by city. Town by town.

At the federal level, an important “tool” used to facilitate the conveyance of properties through land banks became available in 2008.

Resulting from the Financial Crisis, Congress passed the Housing and Economic Recovery Act of 2008. The Housing and Economic Recovery Act appropriated $4 billion to address abandoned and foreclosed properties.

The Housing And Economic Recovery Act of 2008 later became the Neighborhood Stabilization Program. Commonly known as NSP.

One year after the NSP went into effect, Congress appropriated an additional $2 billion to address vacant and abandoned properties. Through the NSP.

The NSP provided the framework – and the funding mechanism – cities relied upon to create programs designed to combat problems arising from increasing numbers of nonperforming properties. A problem amplified by the Financial Crisis.

One approach used in St. Louis to lessen neighborhood blight was the Dollar House Program. To provide the Dollar House Program with inventory, the LRA placed properties in the Program which were owned by the LRA for at least five years.

The Dollar House Program provided owner-occupant applicants with an opportunity to inspect LRA homes. Upon completing inspections, buyers then established rehab budgets. After which, buyers were able to submit their applications to the LRA.

Buyer applications underwent board review. Should a buyer have been deemed to have met Program qualifications, with board approval, within 120 days buyers were expected to, a) stabilize the home, b) improve the facade, and c) follow building codes.

Renovation of Dollar House Program homes needed to be completed within 18 months. Furthermore, the buyer of the LRA home was required to live in their home for at least three years. Once they completed the rehab.

The LRA held a quitclaim deed to properties. Enabling the LRA to regain possession of properties should requirements established by the LRA not be met by buyers. The LRA was able to extend timelines for rehabs which took longer than 18 months to complete.

Buying a distressed home in St. Louis? Buying vacant land in St. Louis? Buying a rundown apartment building in St. Louis?

Some perspective…

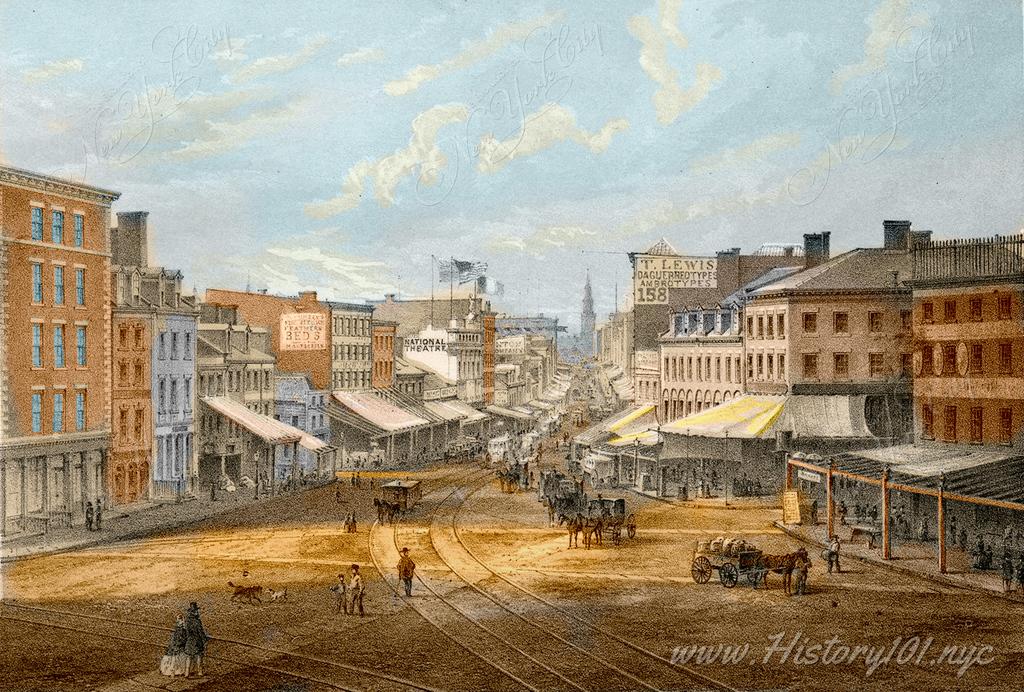

Long, long ago, John Jacob Astor saw something he liked in an overlooked, sneered-upon, not-too-desirable piece of land. That then nonperforming piece of land that John Jacob Astor liked – then purchased – proved to be a decision which anchored his trajectory towards becoming America’s first multi-millionaire. This was a piece of land all know quite well.

Where was this land located?

Beginning in 1799, John Jacob Astor began to acquire vast amounts of land in New York City. Astor went on to become New York’s biggest landlord. Astor owned land in what today we know to be Times Square. And the East Village.

John Jacob Astor’s real estate was the backbone to his wealth.

When John Jacob Astor began buying Manhattan real estate, the population of New York City was 60,000. Fifty years later, New York City’s population exceeded 500,000.

“Buy on the fringe and wait. Buy land near a growing city! Buy real estate when other people want to sell. Hold what you buy!” – John Jacob Astor